Sending money across borders used to mean a trip to the bank, a stack of paperwork, an exchange rate you could not see, and fees that quietly ate into whatever you were trying to send. For the millions of people supporting family abroad, paying overseas tuition, or covering expenses in another country, that friction adds up fast. A wave of digital fintechs has set out to fix it, and one of the names that keeps coming up for its refreshingly simple pricing is Paysend.

Paysend is a UK-based global money transfer service that lets you send money internationally to bank cards, bank accounts and digital wallets in more than 100 countries, usually for a small, flat fee and with most transfers arriving in seconds. Its headline pitch is predictability: you see the cost upfront, the exchange rate is locked in, and the fee does not balloon with the amount you send. In this review, we will break down exactly how Paysend works, what it really costs once you account for exchange rates, how fast and safe it is, how it compares with rivals like Wise and Remitly, and where it falls short — so you can decide whether it is the right way to move your money.

Paysend Review 2026: Is This Flat-Fee Money Transfer App Worth It?

What Is Paysend?

Paysend is a financial technology company founded in the United Kingdom in 2017, built specifically to make international money transfers faster, cheaper and simpler than traditional banks. It now serves around 7 million customers worldwide and focuses on cross-border transfers for both individuals and businesses. Rather than the opaque, percentage-based pricing common in the industry, Paysend built its reputation on a low, fixed transfer fee that stays the same no matter how much you send.

The service works largely through card networks. Using technology from Mastercard, Visa and UnionPay, Paysend can move money directly from your card to a recipient's card, bank account or digital wallet, and in some corridors to a mobile number or for cash pickup. You manage everything through the Paysend app or website, and the whole process — from signing up to sending your first transfer — is designed to take just a few minutes.

On the trust front, Paysend is well credentialed. It is regulated by the UK's Financial Conduct Authority and registered with FINTRAC in Canada, is PCI DSS certified for handling card data, and in the United States operates as a licensed money transmitter. It holds an Excellent rating of around 4.3 from more than 32,000 reviews on Trustpilot, which is strong for the remittance category.

Why Paysend Stands Out

In a crowded money-transfer market, Paysend earns attention through a handful of genuine strengths that suit everyday senders.

A simple, predictable flat fee: Where many providers charge a fixed amount plus a percentage of your transfer, Paysend typically charges one small flat fee that does not change with the amount. Sending the equivalent of 500 or 5,000 costs the same fixed fee, which makes the pricing easy to understand and predictable every time.

Genuinely fast delivery: Speed is a core promise. Paysend reports that around 95% of transfers are completed in seconds, with money often reaching the recipient's card almost instantly. Some transfers to bank accounts can take up to three business days depending on the receiving bank, but for card-to-card transfers the experience is usually very quick.

Flexible ways to send and receive: You can send money from your card to a recipient's card or bank account, to digital wallets, and in some corridors to a mobile number or for cash collection. Where the destination country allows it, recipients can even choose which currency they receive, which adds useful flexibility for families spread across different systems.

Serious security and regulation: Transfers run over major certified payment networks, with two-factor authentication, strict identity verification and continuous fraud monitoring. Combined with FCA regulation and PCI DSS certification, it gives Paysend a solid credibility footing for a service handling your money across borders.

Key Features That Matter

Beyond the headline pitch, these are the features that shape what using Paysend actually feels like.

Flat, Upfront Transfer Fees

The defining feature is the fixed transfer fee, which typically runs around £1 in the UK, €1.50 in the eurozone, or roughly $1.99 in the US, depending on where you are sending from. For most corridors this fee stays flat regardless of the transfer amount, which is what makes Paysend so appealing for larger sends. You always see the exact fee before you confirm, with no surprise deductions appearing later — though a handful of corridors do use variable fees based on the amount, so it is worth checking your specific route.

Card-to-Card and Multiple Payout Methods

Paysend was an early pioneer of card-to-card international transfers, letting you send straight from your bank card to a recipient's card number. Beyond that, you can pay out to bank accounts and digital wallets, and in certain corridors send via a mobile number using a Paysend link or arrange cash pickup. That range of options means you can usually reach a recipient in whatever way is most convenient for them.

Fast, Mostly Instant Delivery

Most Paysend transfers land in seconds, which is a major advantage when someone is waiting on funds. The company states the large majority of transfers arrive almost immediately, with the exchange rate locked in at the moment you send so the amount cannot shift mid-transfer. Delivery to some bank accounts can take longer due to the receiving bank's own processing and compliance checks, but the card-to-card path is consistently quick.

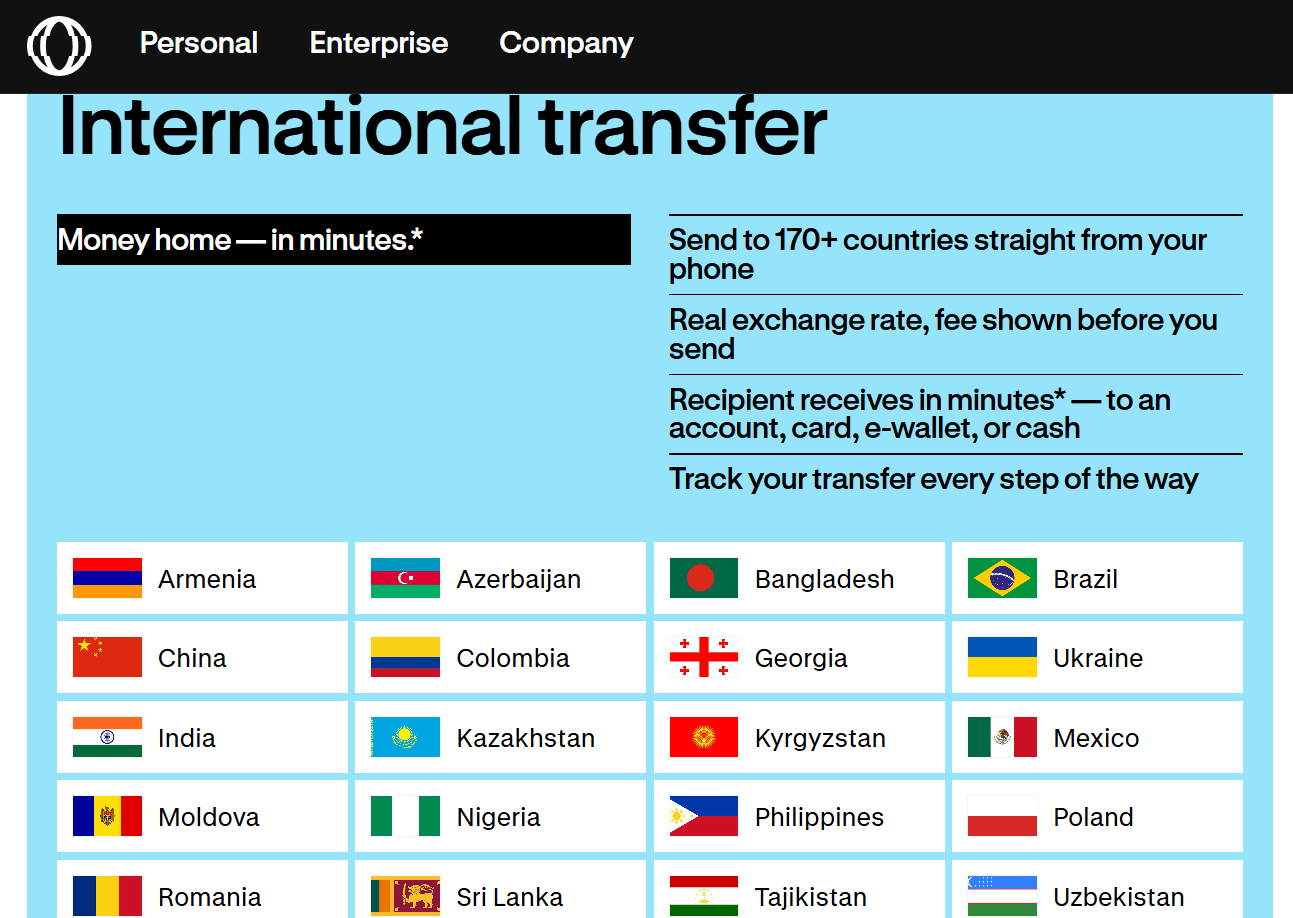

Broad Global Reach

Paysend's disbursing network reaches more than 100 countries across Europe, Asia, Africa and the Americas, covering many of the busiest remittance corridors. It is important to note the asymmetry, though: while you can send money to a very wide list of destinations, outbound transfers can only be started from around 49 supported sending countries. So the country you are sending from matters as much as where the money is going.

Bank-Grade Security and Regulation

Every transfer benefits from PCI DSS-compliant handling of card data, two-factor authentication and active fraud prevention that monitors transactions. Paysend complies with anti-money-laundering rules and is regulated in multiple jurisdictions, including by the FCA in the UK. These protections are the reason a service moving money internationally can be trusted with sensitive payment details.

Referral Rewards and First-Transfer Offers

Paysend runs an invite programme that rewards you when friends you refer make transfers — commonly around £1, €1.50 or $2 per qualifying transfer, for a set number of transfers in the first year, credited straight to your account. New customers can also often claim a first-transfer offer with zero fee and a special exchange rate, which makes trying the service low-risk. Promotional terms change, so check the current offer before you sign up.

Paysend Fees and Pricing Explained

Signing up for Paysend is free, and there is no subscription — you simply pay per transfer. The important thing is to understand the two parts of what a transfer costs: the flat fee and the exchange-rate margin. Here is how it breaks down.

| Charge | Amount (approx.) | Notes |

|---|---|---|

| Transfer fee | ~£1 / €1.50 / $1.99 (varies by region) | Flat per transfer on most corridors regardless of amount; some corridors use a variable fee based on the amount |

| Exchange-rate margin | ~1.5% built into the rate (varies) | Not the mid-market rate; the margin is baked into the quoted rate and locked at the time you send |

| First-transfer offer | Often zero fee + special rate | Promotional, new customers only, time-limited; check current terms |

| Third-party charges | Varies | Your funding bank or the recipient's bank may add their own fees, outside Paysend's control |

A note on the figures: the fees above are approximate and quoted in several currencies because they vary by your sending country, and the exchange-rate margin varies by currency and corridor. All of it is accurate as a general guide as of our research date, but always confirm the exact fee and the final receive amount live in the Paysend app before you send.

How Paysend Compares

Paysend competes with a strong field of money-transfer services, each with a different emphasis. Wise is built around the true mid-market rate, Remitly focuses on remittances with flexible speed options, and Western Union offers an unmatched cash-pickup network. Here is how they line up.

| Feature | Paysend | Wise | Remitly | Western Union |

|---|---|---|---|---|

| Fee model | Low flat fee | Low percentage fee | Varies by corridor and speed | Often higher, varies |

| Exchange rate | Mid-market + ~1.5% margin | True mid-market rate | Margin built into rate | Margin built into rate |

| Delivery speed | Mostly instant | Often instant, varies | Express or economy options | Minutes to days |

| Global reach | 100+ destinations | 140+ countries | Broad remittance corridors | 200+ countries |

| Standout payout | Card-to-card transfers | Multi-currency account + card | Home delivery + cash pickup | Huge cash-pickup network |

| Best for | Small, frequent flat-fee sends | Best rate on larger amounts | Family remittances | Cash pickup anywhere |

The takeaway: Paysend shines for smaller, regular transfers where its flat fee and instant card-to-card delivery are hard to beat. If you are moving larger sums and want the best possible exchange rate, Wise's true mid-market pricing often wins. Remitly is a natural pick for family remittances with flexible speed and payout choices, and Western Union remains unmatched when the recipient needs to collect physical cash. Match the tool to the transfer rather than assuming one service is best for everything.

Pros and Cons of Paysend

No transfer service is perfect, so here is the honest, balanced view of Paysend's strengths and weaknesses.

Simple, predictable flat fee: One low fixed fee that does not scale with the amount makes costs easy to understand, especially for larger transfers.

Fast, mostly instant transfers: The large majority of transfers arrive in seconds, which matters when someone is waiting on the money.

Flexible payout options: Card-to-card, bank account, digital wallet, mobile number and cash pickup in supported corridors give recipients real choice.

Strong security and regulation: FCA regulation, PCI DSS certification, 2FA and fraud monitoring make it a trustworthy option for cross-border transfers.

Transparent, upfront pricing: You see the fee and the locked exchange rate before confirming, with no hidden deductions appearing afterward.

Exchange-rate margin, not mid-market: Paysend adds a markup to the rate, so on larger transfers a mid-market provider like Wise can work out cheaper overall.

Limited sending countries: While it pays out to 100+ destinations, you can only send from around 49 supported countries, which excludes many senders.

Verification can be slow: Identity checks can take anywhere from a few hours to a few days, and larger amounts often trigger stricter documentation.

Modest transfer limits: Limits are tiered by verification level and are relatively low, making the service better suited to smaller transfers than very large ones.

Fewer account features than before: Paysend has narrowed its focus, and cards and multi-currency accounts are no longer offered to new users, so it is now geared toward straightforward transfers rather than a full financial hub.

Who Should Use Paysend?

Paysend is a great fit for people who send smaller amounts abroad regularly — supporting family, covering recurring expenses or sending gifts — and who value a predictable flat fee and fast, card-to-card delivery. It suits anyone who wants a simple, no-frills transfer app with upfront pricing rather than a complicated financial platform, and it is especially convenient when the recipient can receive money directly to a card. The referral rewards and first-transfer offer also make it low-risk to try.

It is a weaker choice in a few situations. If you are moving large sums where the exchange-rate margin adds up, a true mid-market provider like Wise may save you more. If you live in a country Paysend cannot send from, it simply will not work for you. And if you want a broader financial toolkit — a multi-currency account, a card, or investing features — Paysend's narrowed, transfer-focused product will feel limited compared with rivals.

How to Get Started with Paysend

Getting started with Paysend takes only a few minutes, and signing up is free. Here is the step-by-step process from account to first transfer.

- Download the Paysend app or go to the website and create a free account with your email — there is no cost to sign up.

- Complete identity verification by providing the required documents; approval can take from a few hours to a few days, so start this early.

- Tap “Send money,” choose whether you are sending to yourself, another person or a business, and enter the recipient's country.

- Pick the payout method — bank card, bank account, digital wallet or another supported option — and add the recipient's details.

- Enter the amount and currencies, then review the fee and the locked exchange rate so you can see exactly what your recipient will receive.

- Choose your funding method, confirm, and send — most transfers arrive in seconds, and you can track the status and download statements in the app.

Future Outlook and Final Assessment

Paysend's direction is toward doing one thing well: fast, low-cost cross-border transfers. Rather than trying to be a full neobank, it has streamlined its consumer offering — winding down cards and multi-currency accounts for new users — while continuing to expand its global reach and grow its business and enterprise payments arm. That focus should keep its core transfer product sharp and competitive, even as the remittance space stays crowded with well-funded rivals.

The honest caveats remain worth repeating. The exchange-rate margin means Paysend is not always the cheapest option for large transfers, sending is limited to around 49 countries, verification can be slow, and limits favour smaller amounts. None of these are dealbreakers for its target user, but they are real trade-offs to weigh against mid-market providers.

Conclusion

Paysend is one of the simplest and fastest ways to send money abroad in 2026. Its low, flat transfer fee, near-instant card-to-card delivery, flexible payout options and strong regulatory footing make it a genuinely appealing choice for everyday international transfers. It is held back by an exchange-rate margin that erodes value on larger sums, a limited list of sending countries, and a narrowed feature set that no longer includes cards or multi-currency accounts for new users — but for its core purpose of quick, predictable remittances, it does the job very well.

If you regularly send smaller amounts to family or friends overseas and want a transparent, no-fuss app that gets money there fast, Paysend is well worth setting up and testing with its first-transfer offer. Check the final receive amount, match it to the transfers you actually make, and it becomes a reliable tool in your financial kit. At AI Solutes, that is exactly what we aim for: helping you find the right tools and make everything easy.

Ready to send money abroad the simple, fast way? Give Paysend a try.

Explore more honest reviews, tutorials and tool comparisons to find the right tech for the way you work and live — at AI Solutes, where we make everything easy.

👉 Sign Up Free: Get Started with Paysend

👉 Our YouTube Channel: youtube.com/@ai-solutes

👉 Our Facebook Fanpage: Facebook

👉 Our X (Twitter): @AISolutes

- Does Airwallex Streamline Corporate Transactions?

- Qlone

- Supercharge Your Agency or SMB with Cloudways Managed Cloud Hosting: Speed, Security and Scalability Unlocked

- Does Skywork AI Maximize Office Productivity? Reviewing the Skywork AI All-in-One Workspace Technology

- GT Omega Prime vs ART: 2025 USA Comparison to Build Your Best Sim Racing Setup