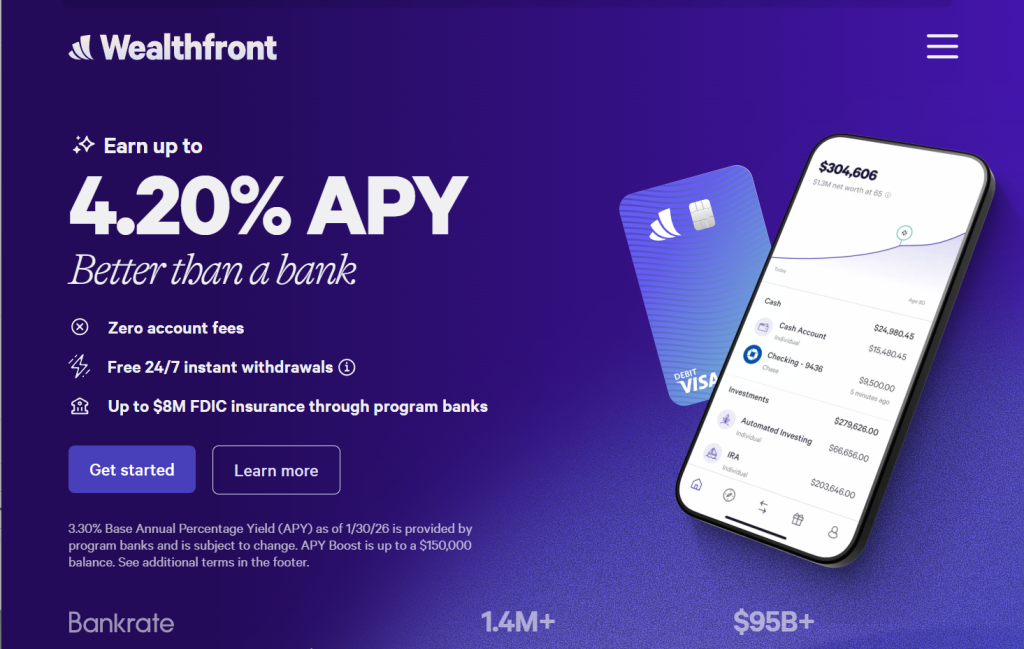

Most people leave their savings sitting in a checking account earning close to nothing while their investments sit in a separate app they rarely check. Wealthfront was built to close that gap: one platform that pays a genuinely competitive interest rate on your everyday cash and automatically manages a diversified, tax-optimized investment portfolio, with instant transfers between the two. Since its founding, Wealthfront has grown into one of the largest independent robo-advisors in the U.S., with more than 1.4 million funded clients and over $95 billion in total assets under management as of 2026. With a flat 0.25% advisory fee, a Cash Account paying 3.30% APY with FDIC coverage up to $8 million, and daily tax-loss harvesting on every balance, it's a genuinely compelling option for hands-off investors who want their money working harder without hiring a human advisor.

But 2026 has also been an eventful year for the company itself. Wealthfront completed its IPO in December 2025, and its stock has traded below its offering price amid reported net deposit outflows, a quarterly net loss, governance questions about its CEO's stake in a new business line, and open SEC investigations. This review isn't going to gloss over that. Below, we break down exactly how Wealthfront's Cash Account and automated investing actually work, the real fee structure, how it compares to Betterment, the honest limitations, and precisely who should — and shouldn't — trust Wealthfront with their money in 2026.

Wealthfront Review 2026: High-Yield Cash and Automated Investing Under One Roof

Overview and Background

Wealthfront started as an automated investing platform — a robo-advisor built on the premise that index-fund investing, when combined with disciplined automation and daily tax-loss harvesting, could match or beat what most human financial advisors deliver, at a fraction of the cost. The company later expanded into cash management with the Wealthfront Cash Account, and today the two products work together as a single ecosystem: park your everyday cash where it earns real interest, then move it into a diversified investment portfolio in minutes when you're ready.

Wealthfront's investing arm is Wealthfront Advisers, an SEC-registered investment adviser, while the Cash Account and brokerage services are offered through Wealthfront Brokerage LLC, a member of FINRA and SIPC. It's important to understand that Wealthfront itself is not a bank — cash deposited into the Cash Account is swept across a network of more than 30 partner banks, which is how the platform is able to offer FDIC insurance coverage up to $8 million for individual accounts (and up to $16 million for joint accounts), far above the standard $250,000 per-depositor limit at a single bank.

In a significant corporate milestone, Wealthfront Corporation completed its initial public offering on December 12, 2025, pricing at $14.00 per share and raising approximately $485 million on the Nasdaq Global Select Market under the ticker WLTH. Going public brings a new layer of public financial scrutiny that private robo-advisors don't face, and it's directly relevant to anyone evaluating the company's stability in 2026.

Why Wealthfront Stands Out in 2026

A genuinely competitive Cash Account with no fees: At 3.30% base APY as of January 2026 — roughly 8 times the national average savings rate — with zero monthly fees, no minimum balance, and no overdraft fees, the Cash Account is a strong home for money you're not ready to invest yet.

FDIC coverage well above the standard limit: By sweeping deposits across 30-plus partner banks, Wealthfront offers up to $8 million in FDIC insurance on individual accounts and up to $16 million on joint accounts — coverage most traditional banks and even many fintech competitors can't match.

Simple, transparent investing fees: Wealthfront charges a flat 0.25% annual advisory fee regardless of balance, with no tiers, no premium upgrades, and no hidden trading, rebalancing, or transfer-out charges — a fee structure that's easy to understand and compares favorably to traditional human financial advisors who typically charge 1% or more.

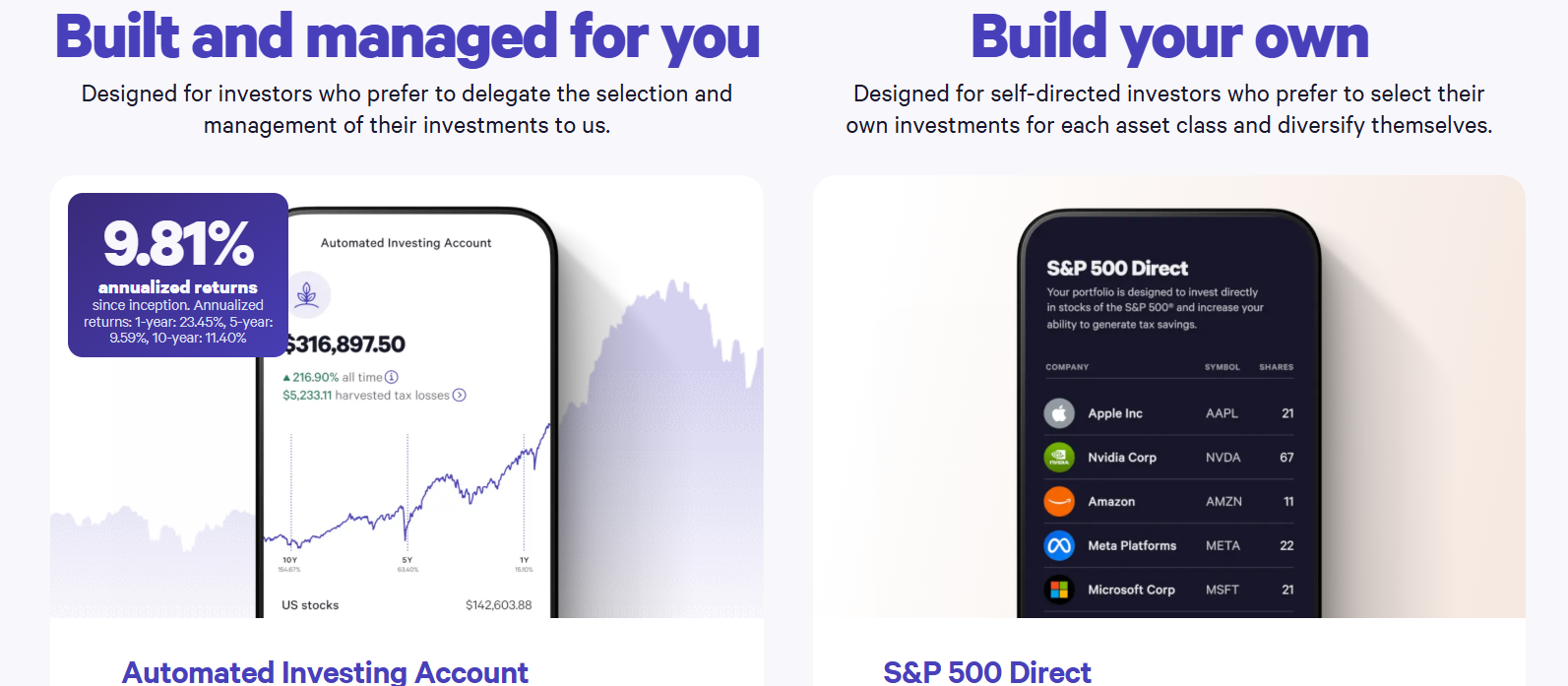

Genuinely sophisticated tax optimization: Daily tax-loss harvesting is applied to every balance, not just accounts above a certain threshold, and clients with at least $100,000 invested can upgrade to stock-level direct indexing — a level of tax sophistication most robo-advisors reserve for much higher account minimums.

One ecosystem for saving and investing: Instant transfers between the Cash Account and investing accounts, a unified financial planning tool called Path that projects retirement readiness and college funding, and an Autopilot feature that automatically sweeps excess cash from an external checking account all reduce the friction of managing money across multiple apps.

Key Features and Technology

Wealthfront's feature set splits cleanly into the Cash Account and Automated Investing Account, plus a few tools that connect the two.

Wealthfront Cash Account

The Cash Account functions as a hybrid checking-and-savings product. It includes a debit card with fee-free access to more than 19,000 ATMs nationwide, reimbursement of up to two out-of-network ATM fees per month (up to $7.50 each), free wire transfers, mobile check deposit, compatibility with apps like Venmo and Apple Pay, and early access to direct deposits — often up to two days ahead of the standard payday. New clients can currently receive a 0.65% APY boost for three months, and successful referrals earn a 0.75% boost, with an additional 0.25% available indefinitely for clients who direct deposit at least $1,000 per month and maintain a funded investing account.

Automated Investing

Wealthfront builds a globally diversified portfolio out of low-cost index ETFs spanning roughly 7 to 8 asset classes, including real assets that some competitors' default portfolios exclude. You can let Wealthfront fully manage the allocation based on your risk profile, or build and customize your own portfolio if you'd rather have more control. Requires a $500 minimum to open.

Tax-Loss Harvesting and Direct Indexing

Daily tax-loss harvesting runs automatically across every account balance, systematically capturing losses to help offset taxable gains elsewhere in your financial picture. At $100,000 or more invested, accounts upgrade to direct indexing, which holds individual stocks rather than ETFs to enable more granular, stock-level tax-loss harvesting — a feature typically reserved for much higher account minimums at competing platforms.

Path Financial Planning

Path is Wealthfront's free planning tool, linking to external accounts to build a holistic view of net worth, projecting retirement readiness, modeling Social Security timing, and estimating college funding needs with real-time scenario adjustments as your situation changes.

Pricing, Plans, and Package Structure

Wealthfront's pricing is genuinely simple compared to most financial platforms: one flat advisory fee for investing, and no fees at all on the Cash Account.

| Product | Cost | Minimum | Notes |

|---|---|---|---|

| Cash Account | $0 (no fees, ever) | $1 to open | 3.30% base APY as of Jan 2026; rate is variable and can change |

| Automated Investing | 0.25% annual advisory fee, flat | $500 | No trading, rebalancing, or transfer-out fees on top |

| Direct Indexing | Included in the 0.25% fee | $100,000 | Stock-level tax-loss harvesting, no extra charge |

Underlying ETF expense ratios still apply on top of the 0.25% advisory fee, as they would with any index-fund-based portfolio — this is standard across the robo-advisor category and not a Wealthfront-specific charge, but it's worth knowing your all-in cost includes both layers. The Cash Account's APY is variable and moves largely in line with the Federal Funds Rate, so the rate you see today isn't locked in indefinitely.

How Wealthfront Compares to Alternatives

| Platform | Advisory Fee | FDIC Coverage (Cash) | Human Advisor |

|---|---|---|---|

| Wealthfront | 0.25% flat | Up to $8M | Not available at any price |

| Betterment | 0.25% flat (Digital) | Up to $2M (Cash Reserve) | Available on Premium tier |

vs. Betterment: The two platforms are close competitors with nearly identical flat advisory fees. Wealthfront tends to win on cash yield, FDIC coverage ceiling, and the frequency of its tax-loss harvesting; Betterment tends to win on small-balance fee structure, access to a human advisor on its Premium tier, and — as of early 2026 — a cleaner current reputational standing without the open SEC investigations or BBB complaints Wealthfront is currently navigating. Which matters more depends heavily on your priorities: pure automation and tax efficiency favor Wealthfront, while wanting the occasional human check-in favors Betterment.

vs. a traditional high-yield savings account: Wealthfront's Cash Account APY consistently outpaces the national average for savings accounts by a wide margin, and the FDIC coverage ceiling is dramatically higher than the standard $250,000 offered at a single bank. The trade-off is that the Cash Account isn't a full checking replacement — there's no cash deposit capability and no physical branch access, so most users will still want a traditional bank account alongside it.

vs. a traditional human financial advisor: A human advisor charging the industry-standard 1% or more of assets under management will cost meaningfully more over time than Wealthfront's flat 0.25%, and won't necessarily deliver better tax-loss harvesting discipline, since daily automated harvesting is difficult for a human to replicate manually. The trade-off is the complete absence of personalized human judgment for complex financial situations — estate planning, business sale proceeds, or highly specific tax circumstances that benefit from a licensed professional's direct involvement.

Pros and Cons

What Users Love

The Cash Account genuinely competes with dedicated high-yield savings products: Users consistently cite the combination of a top-tier APY, zero fees, and unusually high FDIC coverage as a rare package that traditional banks and even most fintech competitors don't match.

Strong app experience: Wealthfront's mobile apps hold 4.8 on the Apple App Store and 4.9 on Google Play, reflecting a genuinely well-designed, easy-to-navigate experience for finding account information, FAQs, and general details.

Seamless movement between saving and investing: Reviewers repeatedly highlight the near-instant transfers between the Cash Account and investing accounts as a genuine convenience advantage over managing separate bank and brokerage relationships.

Sophisticated tax tools at an accessible entry point: Daily tax-loss harvesting on every balance and direct indexing at a $100,000 threshold (rather than $500,000-plus at some competitors) genuinely stands out among independent expert reviews of the robo-advisor category.

Limitations Worth Knowing

Open post-IPO securities investigations and a BBB F rating: These are documented, currently unresolved concerns worth actively monitoring through public SEC filings rather than dismissing, particularly if you're considering moving a significant portion of your assets to the platform.

No human advisor access at any price: If your financial situation involves genuine complexity — a business sale, significant estate planning needs, or highly specific tax scenarios — Wealthfront's fully automated model has no path to a licensed human advisor, regardless of your account balance.

Not a true checking account replacement: No cash deposit capability, no physical branches, and limited customer support hours (7 a.m. to 5 p.m. PT, Monday through Friday, no weekend availability) mean most users will still need a traditional bank account alongside the Cash Account.

No overdraft coverage: Wealthfront simply rejects any transaction the account balance can't cover — there are no overdraft fees, but also no safety net, so you need to actively track your balance to avoid a declined payment.

Account lockout reports: Some user reviews describe experiences with accounts being locked, which can be a genuine inconvenience if it happens while you need timely access to funds.

Who Should Use Wealthfront

Hands-off investors comfortable with a fully digital adviser: If you want a diversified, tax-optimized portfolio managed automatically without paying 1%-plus to a human advisor, and you're comfortable never speaking to a licensed person about your account, Wealthfront's structure fits well.

Savers with balances above $250,000: The $8 million FDIC coverage ceiling is a real advantage for anyone holding cash reserves large enough to exceed standard single-bank insurance limits.

Anyone wanting one ecosystem for cash and investing: If juggling a separate bank and brokerage app feels like unnecessary friction, Wealthfront's instant transfers and unified Path planning tool genuinely simplify day-to-day money management.

Investors approaching $100,000 who value tax efficiency: Direct indexing's stock-level tax-loss harvesting becomes available at a meaningfully lower threshold than many competitors, making Wealthfront an attractive option as your portfolio grows.

Not the right fit: Anyone who wants regular access to a human financial advisor, needs cash deposit capability or branch banking, has complex estate or business-related financial planning needs, or is uncomfortable with the current open securities investigations and BBB rating should weigh those factors carefully or consider a competitor with a longer, more settled public track record.

Getting Started: Step by Step

- Open a Cash Account first. With just a $1 opening deposit and no fees, this is a genuinely low-risk way to experience Wealthfront's app and interface before committing to investing.

- Set up direct deposit if eligible. Redirecting your paycheck can unlock the indefinite 0.25% APY boost, provided you also maintain a funded investing account, and gets you early access to your paycheck up to two days ahead of schedule.

- Enable Autopilot for excess cash. Connect an external checking account and set a threshold so idle cash automatically sweeps into your higher-yield Wealthfront Cash Account without manual transfers.

- Open an Automated Investing Account once you hit $500. Decide whether to let Wealthfront fully manage your portfolio based on your risk profile, or build your own allocation if you want more direct control.

- Run your numbers through Path. Link your external accounts to get a full picture of your net worth and retirement trajectory before making any larger financial decisions.

- Monitor the current investigations before scaling up. If you're planning to move significant assets to Wealthfront, check for updates on the open SEC investigations through public filings before committing beyond what you're comfortable with.

- Set up two-factor authentication. Enable this and biometric login where available to add an extra layer of account security.

Tips for Getting Maximum Value

Stack the new-client and referral APY boosts if you can — both can apply to your Cash Account and meaningfully increase your rate for the first three months. Keep a traditional bank account for daily spending and cash deposits alongside Wealthfront, since the Cash Account is genuinely better suited as a high-yield savings destination than a full checking replacement. If your invested balance is approaching $100,000, understand how direct indexing changes your tax-loss harvesting before you cross that threshold, since it shifts your holdings from ETFs to individual stocks. Track your Cash Account balance actively since there's no overdraft coverage — a declined transaction is inconvenient but at least fee-free, so it pays to know your balance before large scheduled payments. And regardless of how attractive the product features look, do your own diligence on the open SEC investigations and BBB complaint history before moving a large portion of your net worth onto the platform — this review is informational, not financial advice, and a licensed financial or tax professional can help you weigh these factors against your specific situation.

Future Outlook and Final Assessment

The underlying product tailwinds remain strong: automated, low-cost investing continues to gain share from traditional human-advisor models, and consumers are increasingly comparison-shopping cash yields the way they once shopped credit card rewards. Wealthfront's scale — 1.4 million-plus funded clients and $95 billion-plus in assets — reflects a genuinely large, established user base that trusts the core product, and its expansion into direct indexing, custodial accounts, and a portfolio line of credit shows continued product investment rather than stagnation.

The honest caveats are real and shouldn't be minimized: the post-IPO stock performance, open securities investigations, and BBB F rating are documented facts as of early 2026, not rumors, and they represent genuine near-term uncertainty about the company even as the underlying product experience remains strong. Within that context, Wealthfront delivers a genuinely well-built, low-cost automated investing and high-yield cash platform — just go in with clear eyes about the corporate-level questions currently unresolved alongside it.

Conclusion

Wealthfront has built a genuinely strong product: a fee-free, high-yield cash account with industry-leading FDIC coverage, paired with a low-cost, tax-sophisticated automated investing platform that holds up well against far more expensive human advisors. Its scale and app-store ratings reflect real, sustained user trust in the core experience. The honest counterweight is a 2026 that's brought real corporate-level scrutiny — a below-IPO-price stock, open SEC investigations, and an unaddressed BBB complaint history — that any prospective client should factor into their decision rather than ignore. Weigh the product strengths against the current corporate uncertainty, confirm live rates and terms before opening an account, and consult a licensed financial professional for anything beyond straightforward saving and investing — making everything easy, one automated dollar at a time.

Ready to put your cash and investments on autopilot?

Explore more honest reviews, tutorials and tool comparisons to find the right tech for the way you work and live — at AI Solutes, where we make everything easy.

👉 Open Account: Get Started with Wealthfront

👉 Our YouTube Channel: youtube.com/@ai-solutes

👉 Our Facebook Fanpage: Facebook

👉 Our X (Twitter): @AISolutes

- Unlock the Power of ElevenLabs AI Voice Generator: Usability, Growth, and Ethical Innovation 2025

- Discover How Doubao AI Is Revolutionizing Enterprise and Consumer Applications with ByteDance

- Unlock Seamless Trips with the Best Global Travel Ticket Booking Apps of 2025

- Does Rawpixel Revolutionize Access to Public Domain Art? A Closer Look at Rawpixel’s Vintage Curation Framework

- Master 10Web AI Website Builder 2026: WordPress Hosting, Speed Booster & eCommerce SEO